Mississippi Car Insurance Requirements in 2026 (Minimum Coverage for Drivers in MS)

Mississippi car insurance requirements mandate 25/50/25 liability coverage. Under MS state law on car insurance, drivers can meet the state's requirements through car insurance, a surety bond, real estate bond, or cash certificate. Failure to comply may lead to fines up to $1,000, license suspension, and SR-22 filing.

Read more

Find the Lowest Car Insurance Rates Today

Quote’s drivers have found rates as low as $42/month in the last few days!

Table of Contents

Table of Contents

Managing Editor

Laura Kuhl holds a Master’s Degree in Professional Writing from the University of North Carolina at Wilmington. Her career began in healthcare and wellness, creating lifestyle content for doctors, dentists, and other healthcare and holistic professionals. She curated news articles and insider interviews with investors and small business owners, leading to conversations with key players in the le...

Laura Kuhl

Sr. Director of Content

Sara Routhier, Senior Director of Content, has professional experience as an educator, SEO specialist, and content marketer. She has over 10 years of experience in the insurance industry. As a researcher, data nerd, writer, and editor, she strives to curate educational, enlightening articles that provide you with the must-know facts and best-kept secrets within the overwhelming world of insurance....

Sara Routhier

Licensed Insurance Agent

Brad Larson has been in the insurance industry for over 16 years. He specializes in helping clients navigate the claims process, with a particular emphasis on coverage analysis. He received his bachelor’s degree from the University of Utah in Political Science. He also holds an Associate in Claims (AIC) and Associate in General Insurance (AINS) designations, as well as a Utah Property and Casual...

Brad Larson

Updated February 2025

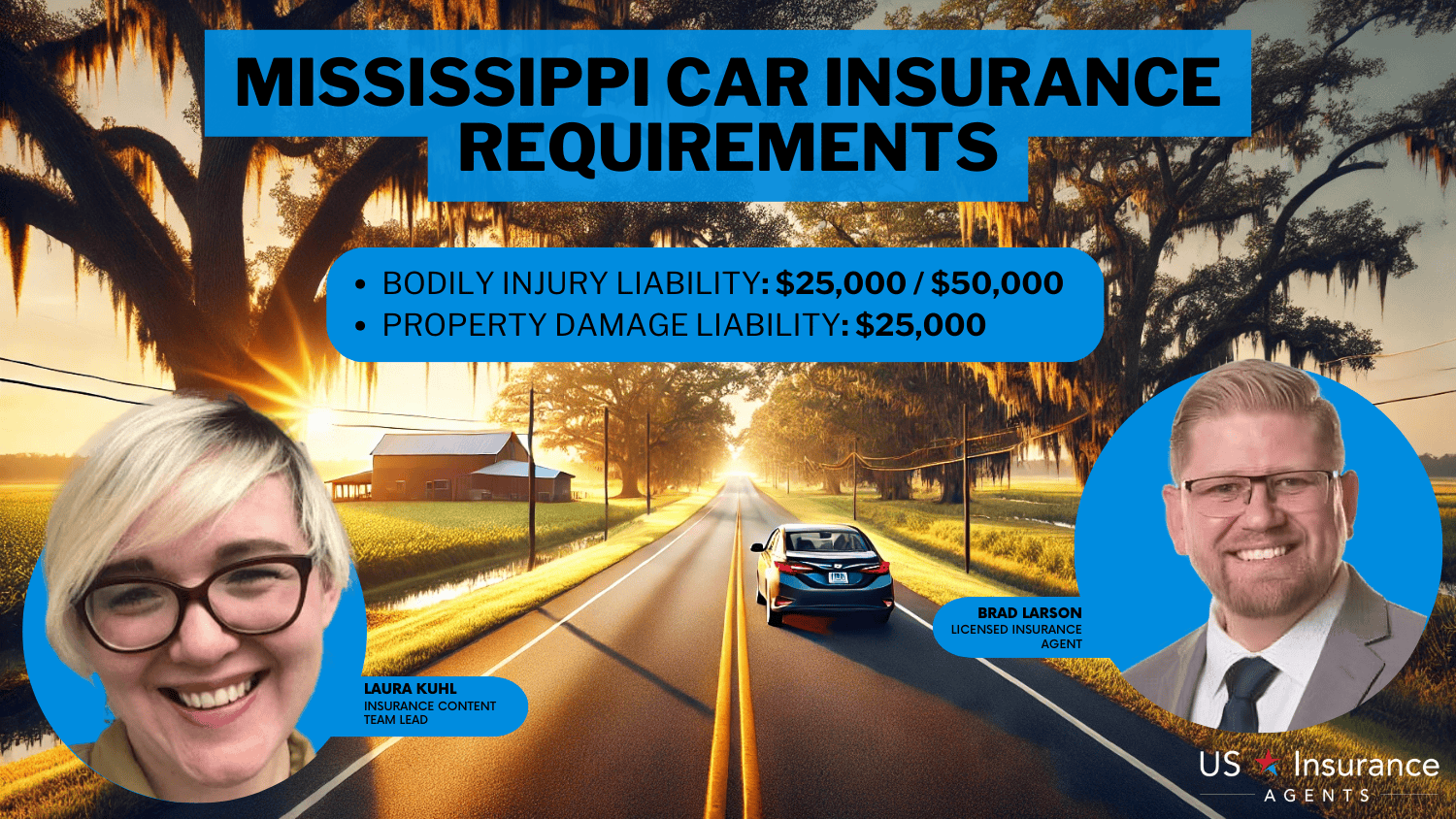

Mississippi car insurance requirements mandate a minimum of 25/50/25 liability coverage, which means $25,000 per person for bodily injury, $50,000 per accident, and $25,000 for property damage. Alternatively, drivers can meet these requirements through a surety bond, real estate bond, or certificate of cash.

Failure to comply may result in fines up to $1,000, a license suspension for up to one year, and misdemeanor charges. Courts may reduce fines and lift suspensions if drivers promptly secure insurance, but penalties can include SR-22 filing, which increases car insurance rates.

Mississippi Minimum Car Insurance Coverage Requirements & Limits

| Coverage | Limits |

|---|---|

| Bodily Injury Liability | $25,000 per person / $50,000 per accident |

| Property Damage Liability | $25,000 per accident |

Since the minimum coverage may not fully protect against damages, consider increasing your limits and adding coverages like collision, comprehensive, or uninsured motorist protection for better financial security.

Enter your ZIP code to compare quotes and find the best coverage options for your needs. Ensure compliance with state requirements by reviewing our Mississippi auto insurance guide.

- Mississippi requires a minimum 25/50/25 liability coverage for all drivers

- Drivers can prove financial responsibility instead of buying insurance

- Failing to meet requirements may lead to fines, license suspension, and charges

MS Minimum Coverage Requirements & What They Cover

Like most states, Mississippi requires drivers to have car insurance. However, Mississippi’s minimum requirements are low and may not adequately cover you. Required auto insurance coverages in Mississippi include:

- $25,000 in bodily injury liability per person

- $50,000 in bodily injury per accident

- $25,000 in property damage liability

Liability coverage pays for damages to others and doesn’t include any protection for you and your vehicle. The bodily injury portion of your coverage pays for medical bills for others, and the property damage pays for other damages, such as car or fence repairs.

Your insurance only pays to the policy limits, leaving you paying for the remaining damages out of pocket in a severe accident. For example, if you cause an accident and the other driver sustains serious injuries, costs quickly exhaust your $25,000 bodily injury limit. Or, if you hit an expensive vehicle, $25,000 in property damage may not be enough to cover repairs.

The injured party can also sue you for additional costs not covered by your insurance. Consider increasing your limits to avoid significant out-of-pocket expenses. Though you’ll pay higher rates, you won’t have to pay substantial costs.

Read more: What states require car insurance?

Free Auto Insurance Comparison

Compare Quotes From Top Companies and Save

Cheapest Car Insurance in Mississippi

Finding affordable car insurance in Mississippi helps you stay compliant with state requirements while keeping costs low.

6,590 reviews

6,590 reviewsCompany Facts

Min. Coverage in Mississippi

A.M. Best

Complaint Level

Pros & Cons

6,590 reviews18,157 reviewsCompany Facts

Min. Coverage in Mississippi

A.M. Best

Complaint Level

Pros & Cons

18,157 reviews 1,734 reviews

1,734 reviewsCompany Facts

Min. Coverage in Mississippi

A.M. Best Rating

Complaint Level

Pros & Cons

1,734 reviewsUSAA, State Farm, and Travelers offer some of the cheapest rates for minimum coverage in the state. USAA typically provides the lowest rates, followed by State Farm and Travelers. You can find coverage starting as low as $20 per month.

- Compare Multiple Quotes: Compare quotes from different insurance providers to secure the best deal. Rates can vary significantly, even for the same coverage. Enter your ZIP code above to see affordable options near you.

- Use Discounts: Take advantage of discounts like safe driving, bundling, or student discounts to further reduce your premium.

- Choose Higher Deductibles: Opt for higher deductibles to lower your monthly payments. Make sure you can cover the deductible if you need to file a claim.

By comparing rates and taking advantage of discounts, Mississippi drivers can find affordable coverage without sacrificing protection.

Penalties for Driving Without Insurance in Mississippi

According to the Insurance Information Institute, about 30% of Mississippi drivers are uninsured, the highest rate in the nation. So, do you need car insurance in Mississippi? Yes, driving without insurance in MS opens up to serious penalties. Penalties for failing to have insurance in Mississippi include:

- Fines up to $1,000

- Driver’s license suspension for up to one year

- Misdemeanor charge

For the first offense, drivers can get a fine of up to $1,000 and a year-long license suspension. However, the court can lift your suspension and reduce your fine to $100 if you acquire insurance within a certain time frame.

The court can also require you to obtain SR-22 coverage, which is a form your insurance company gives the state showing you carry the minimum amount of car insurance. Though the form is relatively inexpensive, an SR-22 increases auto insurance rates, so Mississippi auto insurance quotes with SR-22 can be double standard rates.

Mississippi Car Min. Coverage Insurance Monthly Rates by City

| City | Rates |

|---|---|

| Batesville | $56 |

| Biloxi | $68 |

| Brookhaven | $62 |

| Clinton | $64 |

| Corinth | $57 |

| D'Iberville | $62 |

| Greenwood | $61 |

| Gulfport | $65 |

| Hattiesburg | $64 |

| Jackson | $70 |

| Laurel | $58 |

| Madison | $65 |

| McComb | $54 |

| Meridian | $62 |

| Natchez | $59 |

| Ocean Springs | $63 |

| Olive Branch | $67 |

| Pascagoula | $66 |

| Petal | $57 |

| Ridgeland | $66 |

| Southaven | $66 |

| Starkville | $61 |

| Tupelo | $63 |

| Vicksburg | $60 |

| Waveland | $55 |

Insurance rates are much higher because insurers view you as a risky driver since you drove without coverage. Although most car insurance infractions don’t appear on your criminal record, breaking the Mississippi auto insurance law is a misdemeanor.

Carry at least the mandatory required Mississippi car insurance to avoid higher rates, fines, and a criminal record. If you have car insurance or proof of financial responsibility but don’t have the forms with you, the court typically allows you to show evidence to avoid penalties.

Read More: Can you lend your car to an uninsured driver?

Other Coverage Options to Consider in Mississippi

Drivers who don’t want to carry Mississippi car insurance have another option: They have the option to forgo insurance after proving they can pay for damages up to the minimum policy limit. For example, drivers must show $75,000 in assets that can pay for damages if needed.

Proof of financial responsibility options include:

- Surety Bond: A surety company issues bonds and covers costs up to the bond’s limit. Then, you’ll pay back the company the amount used to pay for damages.

- Real Estate Bond: Drivers show they have real estate holdings worth enough to cover Mississippi state minimum car insurance requirement. In addition, drivers must show $150,000 in equity or stock.

- Certificate of Cash: This document shows you have money equal to at least the minimum amount of required insurance deposited with the Mississippi state treasurer. This money is unavailable to you unless used to pay for damages.

Remember that you won’t have to pay for damages up to your policy limits with a car insurance policy. With a financial responsibility form, you’ll pay for all damages yourself.

While you won’t have car insurance costs, you’ll probably lose money in the long run by paying out of pocket for all damages. Understanding your car insurance can help you assess coverage options to avoid significant financial risks.

Other Car Insurance Coverages in MS

While Mississippi only requires liability insurance, there are other coverages you should consider adding to your policy to be fully protected. Additional car insurance coverages include:

- Collision Coverage: Collision coverage pays for damages to your vehicle if you’re in an accident.

- Comprehensive Coverage: This coverage pays for damage to your vehicle unrelated to an accident, such as fire, theft, vandalism, and hail.

- GAP Coverage: GAP coverage pays for the difference between what you owe on your car and its worth. GAP insurance costs typically range from $20 to $40 annually or $500 to $700 if purchased through a dealership.

- Uninsured/Underinsured Motorist Coverage: If an uninsured driver hits you, your uninsured motorist coverage kicks in to pay for damages. Like uninsured motorist coverage, underinsured motorist coverage pays for damages if a driver with inadequate coverage hits you.

- Medical Payment and Personal Injury Protection: These coverages are very similar, paying for medical and related costs, such as doctor bills, lost wages, and child care.

- Rental Car Coverage: Rental car coverage pays for a vehicle for you to drive while your vehicle is in the shop for a covered claim. You can check “Best Car Insurance for Rental Reimbursement Coverage” to explore coverage options that protect against out-of-pocket expenses.

- Roadside Coverage: This coverage provides service if you have car trouble, including jump starts, tire changes, and fuel delivery.

How much insurance coverage do I need? The coverage you need depends on your vehicle and financial situation. For example, if you have an older car and can afford to make repairs yourself, you could skip collision and comprehensive coverages.

However, experts recommend full coverage insurance, which combines your state’s mandatory coverages with collision and comprehensive insurance. Although full coverage is more expensive, it provides the most protection. If you have a car loan or lease, you may not have an option for car insurance coverage. Typically, lenders require collision, comprehensive, and GAP coverages in addition to your state’s mandatory coverage.

Free Auto Insurance Comparison

Compare Quotes From Top Companies and Save

Mississippi Car Insurance and Compliance Tips

Mississippi car insurance requirements mandate carrying at least 25/50/25 in liability coverage. If drivers don’t want car insurance, they can show financial responsibility through a surety bond, real estate bond, or certificate of cash.

While Mississippi’s required limits are low, it pays at least a portion of damages. However, drivers who choose to carry bonds or a certificate of cash must pay for all damages out of pocket.

Kristine Lee Licensed Insurance Agent

Failing to meet Mississippi minimum insurance requirements results in fines up to $1,000, license suspension for up to a year, and a misdemeanor on your record. To avoid penalties and higher rates, consider securing coverage from the best Mississippi auto insurance providers for compliance and protection.

Mississippi drivers should consider increasing limits and adding coverages to be better protected. Although rates are higher, so is coverage, leading to fewer out-of-pocket expenses. Enter your ZIP code to explore coverage options and ensure full compliance.

Frequently Asked Questions

What is the minimum auto insurance coverage in Mississippi?

What is the minimum insurance coverage in Mississippi? Mississippi law requires drivers to carry at least 25/50/25 liability coverage—$25,000 for bodily injury per person, $50,000 per accident, and $25,000 for property damage.

What is full coverage insurance in Mississippi?

Full coverage typically combines liability, collision, and comprehensive coverage. It may also include uninsured/underinsured motorist protection and medical payments coverage.

What is the minimum amount of insurance most states require drivers to have?

Most states require liability coverage with limits similar to 25/50/25 minimum car insurance in Mississippi. Enter your ZIP code to find coverage options that meet other states and Mississippi insurance requirements.

What is the average cost of auto insurance in Mississippi?

How much is car insurance in Mississippi? Car insurance rates vary, but minimum coverage in Mississippi can cost around $30–$60 per month, depending on factors like age, driving history, and vehicle type.

Is it illegal to drive without insurance in Mississippi?

Does Mississippi require car insurance? Yes, driving without insurance in Mississippi is illegal and can lead to fines up to $1,000, a license suspension, and potential SR-22 requirements.

What is the liability insurance coverage in Mississippi?

What minimum amount of automobile liability insurance is required in Mississippi? Mississippi’s minimum liability coverage is 25/50/25, covering injuries and property damage to others if you’re at fault in an accident.

Which insurance coverage is required by law in most states?

Most states, including Mississippi, require liability insurance as the minimum mandatory coverage.

How much is an insurance license in Mississippi?

Obtaining an insurance license in Mississippi typically costs between $100 and $200, including application and examination fees.

What is the best car insurance in Mississippi?

The best car insurance varies based on individual needs. USAA, State Farm, and Travelers often offer competitive rates and coverage options in Mississippi.

What is the insurance code 83-9-5 in Mississippi?

Mississippi Insurance Code 83-9-5 governs the provision of certain health insurance benefits, including Mississippi auto insurance requirements for coverage related to specific services.

What does full coverage include?

Do you need insurance to register a car in Mississippi?

Related Articles

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.